OTTAWA – Federal efforts to map parts of the country facing the highest risk of flooding are not on track to finish by the 2028 target date and don’t account for the effects of climate change, Canada’s environment watchdog said in a new report.

It was one of five reports issued by environment commissioner Jerry DeMarco and auditor general Karen Hogan on Monday — which also included probes of Canada’s avian flu response, First Nations funding, the climate resilience of federal assets, and how well the government accommodates accessibility needs in the public service.

The flood mapping report found the flood risk awareness portal under development at the Public Safety department does not consider how climate change is affecting flood patterns.

“Flood hazard maps must integrate climate change projections; otherwise, the data are not accurate enough to guide long-term decisions, such as where to build homes or develop infrastructure,” the report said.

The risk ratings were generated using present-day assumptions and the audit found that because the government used a private sector contractor to create a proprietary system, it was not able to adjust the model.

The audit also looked at efforts to map high-risk flood areas at the Natural Resources department.

The department identified 200 areas at high risk of flooding in 2022 but the audit found it did not monitor whether the mapping projects actually covered those priority areas.

As a result, the audit said, less than half of the 131 mapping projects cover the high-risk areas identified after that 2022 analysis. Only 11 of those maps had been posted to the Canada flood map inventory.

Flood relief efforts cost the federal government an average of $230 million a year between 2016 and 2025. That average cost is rising as a result of climate change and population growth.

The national risk profile found about 80 per cent of highly populated areas of the country are at least partially in flood hazard zones.

DeMarco is recommending the government create user-friendly, interactive flood maps to ensure people can prepare.

The audit notes federal investments in homes and infrastructure, “including those announced in Budget 2025, could be planned and designed with climate readiness in mind by using reliable and actionable flood hazard information.”

The audit also says the government needs to work with provinces and territories to monitor high-risk areas.

The government says it has accepted all recommendations.

The Government of the Northwest Territories (GNWT) is getting its affairs in order as it outlined its wildfire forecast and readiness for the 2026 wildfire season on Tuesday afternoon.

One of the factors raised during the briefing was the drought conditions the territory has been facing for the last few years Regarding those conditions, Jason Currie, wildfire operations manager with the Department of Environment and Climate Chamge (ECC), said those conditions will continue, but thatit’s lessened a bit.

“There is some recovery from the drought, but we didn’t get to rain last fall, which would have played a lot into recovery,” he said.

Currie said with the drought, fires burn much deeper into the ground, making them more challenging to fully extinguish.

According to the GNWT, in Fort Simpson between May and August 2025, just 40 per cent of average rainfall fell. In Fort Liard, it was 33 per cent.

Additionally, Currie said that as the La Nina, a Pacific Ocean pattern that brings cooler temperatures across the NWT, is expected to switch to El Nino, which will bring warmer temperatures.

That means the NWT could heat up, further complicating the wildfire season, he noted.

As part of the GNWT’s operational readiness, infrared scanning missions on large fire perimeters to seek and destroy hot spots have been done. These scanning missions identified spots near Fort Providence, Whati, Fort Liard, and Jean Marie River.

Territorial winter precipitation for the 2025-26 winter season has been roughly average with some notable highs and lows in various regions. For example, Fort Smith saw 141 per cent of its normal snow fall for November, and 184 per cent during February.

Hay River saw 66 per cent of its normal snow fall during November, and 83 per cent in January, but also saw 119 percent in December and 111 per cent in February.

Fort Liard saw only 63 per cent of its normal snow fall in November, 51 per cent in January, and 67 per cent in February. In total, Fort Liard only saw 79 per cent of its normal snow fall this season.

Fort Simpson saw 89 per cent of its normal snow fall for the entire winter season, and Yellowknife and Norman Wells saw 91 and 93 per cent respectively over the same timespan.

The GNWT also conducted snow surveys that measure the accumulated snow on the ground, and that provide insight on how much water will be released into the ground when the snow fully melts.

Yellowknife leads the figures with 163 per cent of its five-year average snow pile-up. Fort Liard had 140 per cent of its average this season and Hay River had 125 per cent. Norman Wells saw the lowest snow pile up this year at only 95 per cent of its five-year average.

According to the GNWT, these snow conditions imply that an early start to the fire season is unlikely. The accumulated snow has the dual effect of added surface moisture and suppressed temperatures.

Currie, who lives in Fort Smith,said there’s still a lot of snow still left on the ground, which he said will most likely delay the fire season.

“It’s good to see that we got snow in the last few years,” he said. “We’ve been well-below average, and that’s kind of dictated what kind of fire season we’ll be having.”

After 13 years advocating tirelessly for an earthquake backstop, the Property and Casualty Insurance Compensation Corporation (PACICC) has been asked to help flesh out exactly what the backstop would look like.

“And the deadline was just seven weeks away!” PACICC president and CEO Alister Campbell writes in the corporation’s latest quarterly Solvency Matters report.

Finance Canada launched a consultation on Feb. 24 to hear ideas on what an earthquake insurance cost-sharing arrangement might look like, following a desktop simulation demonstrating the scope and scale of Canadian earthquake exposure in British Columbia and Quebec. The federal government imposed a deadline of Apr. 10.

“As I write this note, we are still developing our full, formal response to the Finance Canada consultation,” Campbell writes. “But the broad strokes are already clear and I am comfortable sharing — at a high level — what we are likely proposing to tell Ottawa.”

One component of the model is that any proposed solution must cover both federally and provincially supervised insurers. “The cost-sharing arrangement needs to be a national mechanism, not just a federal one — in order to fully mitigate systemic writes,” Campbell says. He notes more than 60% of Quebec personal property insurance and 20% of B.C. personal property insurance is currently underwritten by provincial insurers.

Quebec-based Desjardins Group is the largest provincially-regulated insurer. The inclusion of provincially regulated insurers in the cost-sharing arrangement is important, says Evan Stubbings, director of government affairs at Desjardins Group.

“What we are looking for as an industry is a backstop and upfront liquidity to pay for those claims, because there is going to be a huge, huge influx when this happens,” Stubbings said last week at Insurance Institute of Canada’s annual CIP Society symposium in Toronto.

Importance of inclusion

Why does it matter that provincially regulated insurers are included?

“We’re part of Desjardins Group, we have some capital. I think we’ll be okay,” Stubbings says. “But smaller players, if they start to fail because they aren’t part of that liquidity solution, the other carriers, including the federal ones, are just going to assume that risk anyways through their PACICC assessments…

“We really wouldn’t be moving the needle whatsoever if we do not include the entire industry.”

PACICC is also proposing a cost-sharing arrangement modelled on the U.S. terrorism backstop TRIA, the Terrorism Risk Insurance Act. It would be structured with a clear trigger or threshold, an appropriate deductible or net retention for the industry, and an upper bound on total government obligation with some sort of “re-coupment” model, Campbell writes.

TRIA provides for a transparent system of shared public and private compensation for certain insured losses. The federal backstop applies only if total industry insured losses exceed the statutory program trigger.

“Careful modelling and analysis will be required to set ‘trigger/thresholds’ and the industry ‘deductible’ in the ‘TRIA-like’ structure,” Campbell writes. “To the extent that any successful design will need to allow insurers ‘to fail’ (as antidote for ‘moral hazard’), there will also need to be accurate modelling to estimate how much failure the system can ‘afford.’

“It seems very possible that the PACICC Systemic Risk Model (encompassing both federal and provincial insurers) will prove to be invaluable in supporting this modelling work.”

A recoupment mechanism will likely be a central element of the arrangement. This will enable the industry to repay funds received from the federal government over a period of time after the major earthquake event, Campbell notes.

Lastly, “it is past time for Finance Canada to formally designate PACICC as a ‘compensation association’ under the federal Insurance Companies Act.”

Desktop simulation to formal consultation

The most recent earthquake developments occurred in mid-December in Ottawa after the Office of the Superintendent of Financial Institutions hosted PACICC and the Insurance Bureau of Canada. The industry engaged federal and provincial stakeholders in a desktop simulation demonstrating the scope and scale of earthquakes in B.C. and Quebec.

That exercise provided modelled estimates for two “scientifically credible” events, and the resulting total ground-up losses and insured losses, as well as an evaluation of the likely damage to strategic infrastructure assets such as airports, ports and power plants. Modelling also included fiscal needs and expected impacts to overall GDP and government revenues.

Desktop simulation participants were shown events that would send PACICC member insurers past the ‘tipping point,’ causing them to fail and fuelling systemic contagion. The success of the simulation prompted the formal consultation.

“We anticipate the next few weeks and months to be quite hectic, as we work with all industry and federal/provincial stakeholders to get to the finish line on design of an effective liquidity backstop mechanism,” Campbell writes. “And it is realistic to assume there will be at least a few more bends in the road before we get there.

“But after 13 years of effort, it is clear that we have never been closer to seeing — and perhaps even being part of — a solution to address this glaring gap in the public infrastructure of Canada.”

Flood risk is making housing less affordable in Ontario by driving up home insurance premiums, according to a new joint study by insurtech MyChoice and digital real estate platform Wahi.

The study analyzed how flood risk is influencing the true cost of homeownership across 39 Ontario cities.

“What we found is a growing disconnect between purchase affordability and ownership costs,” MyChoice tells Canadian Underwriter.

Each city was assigned a flood risk score on a scale of 1 (lowest) to 5 (highest). Comparing 2024 and 2026 data using a standardized homeowner profile, the information was combined with RPS-Wahi Home Price Index data and MyChoice insurance datasets to examine how premiums are evolving in higher-risk areas, and what that means for housing affordability.

According to the study, Ajax (4.6/5) is the province’s highest flood-risk city. It saw premiums rise 26%, from $1,022 to $1,290 between 2024 and 2026. “While insurance still represents a smaller share of mortgage payments at 3%, the rate of increase highlights how quickly affordability dynamics can shift in high-risk urban markets,” the report says.

Ottawa (4.5), Mississauga (4.4) and Toronto (4.3) also recorded steady premium increases, ranging from 12% to 18%. But higher home values in these markets continue to keep insurance-to-mortgage ratios relatively low (between 3% and 4%).

Sarnia (4.1) presents a similar pattern, with insurance costs making up 6% of mortgage payments, despite more moderate premium growth (up 9%). Brantford (4.2) and Brockville (3.8) also fall into this category, with insurance accounting for 5% to 6% of monthly costs.

The situation is different in Northern Ontario. “While flood risk scores are lower on average, cities such as Thunder Bay, North Bay, and Sault Ste. Marie are seeing some of the fastest premium increases and highest insurance-to-mortgage ratios in the province,” MyChoice says.

Study methodology

For consistency, the study focused on quotes reflecting a standardized homeowner profile: a 35-year-old male or female with a clean claims history, currently insured, non-smoker, living in a semi-detached or detached three-to-four bedroom home (2,000–2,500 sq. ft.). Each property was assumed to have monitored fire and burglar alarms, at least one fire extinguisher, a $1,000 deductible, $1 million liability coverage, and an Enhanced Water Protection package.

To illustrate how flood risk translates into changes in insurance costs and overall housing affordability pressures across Ontario markets, the report calculates the monthly insurance-to-mortgage ratio for each city. It factored in local home values, standard mortgage assumptions (five-year fixed term, 20% downpayment, and prevailing interest rates in 2024 and 2026), and average home insurance premiums — “providing a clear picture of how rising insurance costs affect homeowners’ monthly budgets.”

Based on the survey results, a clear divide is emerging across Ontario, MyChoice says. In higher-priced markets, rising insurance costs remain diluted by home values. In more affordable markets, particularly those with elevated flood risk, insurance is already taking a significantly larger share of monthly housing costs.

“Affordability isn’t just about what you pay for a home anymore, it’s increasingly about what it costs to protect it. Rising home insurance rates in flood-prone areas might be pushing potential home buyers out of those markets,” MyChoice CEO Aren Mirzaian tells CU.

Climate implications

This shift is being driven by climate exposure and unlike in the U.S., Canada still lacks a national flood insurance backstop, leaving more risk priced directly into premiums, MyChoice says.

Quebec has been gradually rolling out provincial flood maps since March. Nationally, Canada’s emergency management minister, Eleanor Olszewski, told Canadian Press last week she can’t guarantee the government will launch the promised National Flood Insurance Program “in the near future.”

Insurance Bureau of Canada’s vice president of federal affairs, Liam McGuinty, toldCU the federal government continues to engage the P&C industry, provinces and territories on the design of the national program. The work includes exploring how a backstop would function alongside expanded flood coverage by Canada’s private home insurance market.

Multiple Canadian Underwriter sources believe Ontario’s auto reforms to be introduced this summer could spark new lawsuits – or even endanger the assets of some insureds.

Ontario has a hybrid private auto insurance system that pays out accident benefits to insured drivers injured in auto collisions. It also has a tort system allowing injured drivers to sue to recover compensation for their injuries from at fault drivers. As of July 1, Ontario is making several mandatory accident benefits optional, including income replacement and housekeeping benefits, so that insured drivers can save money on premium by opting not to receive optional benefits.

However, the industry is wondering if any savings gained from the optional accident benefits side may in fact increase costs on the tort side.

Now, and after July 1, Ontario drivers are required carry minimum liability coverage providing protection in the event they’re found legally responsible for injuries or damages to others, notes Michelle Dodokin, head of auto insurance supervision at the Financial Services Regulatory Authority of Ontario (FSRA).

“In the Ontario system, the right to sue is limited to accidents causing certain serious or permanent injuries as defined by the Insurance Act,” she tells CU. “The right to sue is based on respective fault for the cause of an accident.”

All Ontario drivers carry a mandatory $200,000 of personal liability insurance that covers drivers for claims against them if they’re at fault in an accident, “against claims for compensation from not-at-fault victims up to that limit,” says David Marshall, who has served as a senior advisor to the Government of Ontario on auto insurance and pension funds.

He says if the claim exceeds $200,000, the driver would be liable to pay the excess “from their personal assets unless they have purchased excess coverage, which is optional.”

He adds most drivers currently purchase about $1 million of personal liability insurance, “So, the risk of losing your home is minimal.”

Industry experts have also raised questions about whether auto policies renewing after July 1 could leave uninsured injured persons, such as pedestrians or cyclists, without access to specific benefits they can currently access through an insured driver’s policy – such as income replacement, housekeeping, dependent care or death benefits. “There is no way to provide them with insurance under the new auto insurance rules in Ontario,” Marshall tells CU. “If they are not at fault and need these benefits, they will have to sue the at-fault driver, which is one of the reasons litigation costs are going to rise.”

Dodokin stresses pedestrians and cyclists would still have access to the mandatory medical and rehabilitation accident benefits.

“Additional coverages such as income replacement may also be available to them through supplementary benefits, such as disability coverage through employer benefit programs. Pedestrians and cyclists may also purchase a driver’s policy, which provides accident benefit coverages to someone that does not own their own vehicle,” she says.

In some cases, uninsured people injured in auto accidents (and who cannot access insurance under the new rules) may be left with no choice but to sue, says Marshall.

“It is important to understand that a person can sue an at-fault driver for economic loss – for example, the cost of health care and wage loss,” he tells CU. “They can also sue for non-monetary loss called ‘pain and suffering,’ but this latter category needs proof that you have suffered a serious permanent injury. And there is also a need to prove that your suffering is worth more than a given deductible which today is about $48,000.”

In practical terms, Marshall says Ontario’s optionality reforms do mean innocent pedestrians or those who don’t have auto insurance, but whose needs exceed the $65,000 mandatory medical coverage (which they can access) will have to hire a lawyer and wait while the legal process runs its course. The same is true for those who experience wage loss.

That can take “two or more years [for them] to get paid,” he notes.

“In the meantime, they will have to pay for medical care [that’s] not covered by OHIP out of their own pocket and suffer wage loss till they can get back to work – unless they also have wage protection through an employer policy,” he says.

He says both the changes, and the “sheer complexity of the new rules,” could increase disputes and litigation.

Dodokin points out FSRA recognizes the insurance coverage changes can create questions for consumers, and that the regulator “collaborated with insurers and brokers to provide clear consumer information materials to ease this transition.”

New Quebec flood zone maps could lead to higher home insurance premiums, coverage limitations and more complex underwriting for flood protection, CAA-Québec warns.

Since March 2026, Quebec’s provincial government has gradually rolled out the new flood maps. These updated maps will have tangible insurance implications for homeowners, condo owners and tenants, CAA-Québec says.

There’s not only a risk of higher insurance premiums, there’s also a possibility that insurance coverage for water damage may no longer be available to people who are now considered to live in flood zones, Suzanne Michaud, CAA Québec’s vice president of insurance, tells Canadian Underwriter.

The new maps could also lead to coverage restrictions.

“We could see restrictions of coverage for specific protections and endorsements, [such] as the ones for backflow of sewage, water damage above ground, flooding, water infiltration through the ground, [and] replacement value,” Michaud says.

Some insurers may also require a check valve, submersible pump, the elevation of equipment such as furnaces and electrical panels, or land development requirements, she adds.

Keep clients informed

How do clients get information on the new flood maps?

Michaud says information is first provided by the Government of Quebec. For now, municipalities and “municipalités regionals de comtés” (MRC – regional county municipalities, or county-like units of government) will receive the first-issued maps. Municipalities and MRCs will then study the maps to be able to answer questions from consumers when the maps are widely released.

“Because it is clear that there will be questions from people who find themselves in the new flood-prone areas,” Michaud says, adding she knows there are “some negotiations with the MRCs and the government about who will be in charge to produce the final version of those maps, because of potential legal effects.”

The Government of Quebec is updating its flood zone mapping to strengthen flood prevention and help communities better manage flood risks. It introduces new regulations and amends existing ones.

The new flood maps differ from the old ones in many ways, Michaud tells CU.

For example, the old maps had two zones based on flood recurrence frequency: 0-20 years (high risk) and 20-100 years (moderate risk). The new mapping is more realistic and easier to understand, considering type of flooding, frequency, water depth and the impact of climate change. It’s broken up into four zones, defined by descriptions and colours, for very high risk, high risk, moderate risk and low risk.

The old maps only considered the probability of flooding, while the new ones consider those likelihoods, as well as depth of water, 25-year frequency and other conditions such as the presence of ice or dams. In addition, the new maps consider historical data, while also taking climate changes into account, and are reviewed every 10 years at a minimum.

National implications

Nationally, Canada’s emergency management minister, Eleanor Olszewski, says she can’t guarantee the government will launch the promised National Flood Insurance Program “in the near future.” Canadian Press reported last week Olszewski told reporters the program is still “top of mind” but it’s complicated to set up.

Liam McGuinty, Insurance Bureau of Canada’s vice president of federal affairs, toldCU the federal government continues to engage the P&C industry, provinces and territories on the design of the national program. The work includes exploring how a backstop would function alongside expanded flood coverage by Canada’s private home insurance market, he says.

A majority of Canadians underestimate their exposure to flood risk, even though flooding remains Canada’s most common and costly natural hazard.

Sixty-two percent of Canadians aren’t concerned about flooding in their home or community, according to new survey data released by Intact Financial Corporation on Apr. 1.

Despite this, federal data shows 80% of major Canadian cities are wholly or partially built on or near floodplains.

Intact’s survey was conducted by Léger among 1,639 Canadians between March 13-16.

The finding highlights Canada’s persistent “national flood risk blind spot,” as Intact calls it, which continues to influence preparedness and insurance uptake.

Many Canadians have yet to take action

With spring thaws accelerating flood risks, Intact is urging Canadians to prepare and reduce their exposure to costly damage from rapid snowmelt and rain, which can overwhelm blocked drains and gutters, leading to pooled water near foundations and seepage into homes.

Simple preventive actions, such as maintaining drainage systems or installing sump pumps, can significantly reduce damage, yet many homeowners have not taken these steps, Intact notes.

Even among those willing to act, “access to trusted professionals is emerging as a notable barrier to risk mitigation,” Intact says. According to the insurer, one in five Canadians cite difficulty securing reliable contractors as among their top three obstacles to taking additional steps to protect their home against extreme weather.

Misplaced focus

The persistent perception gap highlighted by Intact’s finding is reinforced by how Canadians think about water-related risks more broadly.

While 2024 saw several significant flooding events across Canada, 2025 was comparatively benign for major flood events.

In quieter years, attention often shifts to more visible or seasonal risks.

Separate industry data shows Canadians are increasingly concerned about winter-related risks such as burst pipes and power outages.

According to First Onsite Property Restoration’s annual property and weather survey, released in December, seven in 10 Canadians are worried about winter storms and power outages, while 68% are concerned about extreme cold and burst pipes.

Despite this, most actual winter damage stems from routine flooding scenarios that involve drain backups and sump pump failures, First Onsite says.

This can include spring snowmelt overwhelming municipal drainage systems, ice damming that forces water back into roofs and walls, and heavy rainfall that exceeds grading or foundation drainage capacity, allowing water to pool and seep into basements. In urban areas, aging infrastructure and limited stormwater capacity can compound the issue, turning moderate rainfall into localized flooding events.

Individually, these incidents may appear minor. But they generate a steady volume of insurance claims every year, with mostly preventable losses that can accumulate significantly across portfolios, even in a year of virtually no headline-grabbing disasters.

The situation sees more Canadians opting to prepare for the risks they notice, and not always for the ones most likely to cause loss.

Bridging the awareness gap

Historically, industry surveys consistently point to awareness gaps, with many Canadians either unaware of their flood risk or assuming they’re not exposed, even when living in flood-prone areas.

The challenge for the industry is managing escalating losses while closing the gap that continues to influence Canadians’ mitigation behaviour and coverage decisions.

In the decade before 2024’s record-breaking catastrophic events, floods have cost insurers on average $800 million a year, according to the Insurance Bureau of Canada.

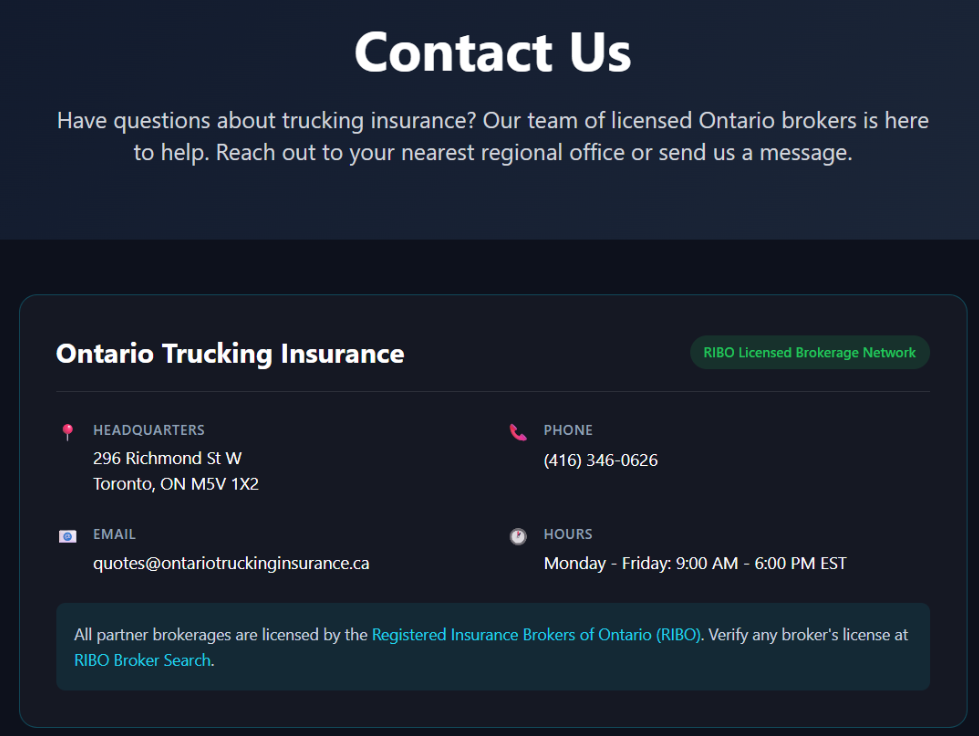

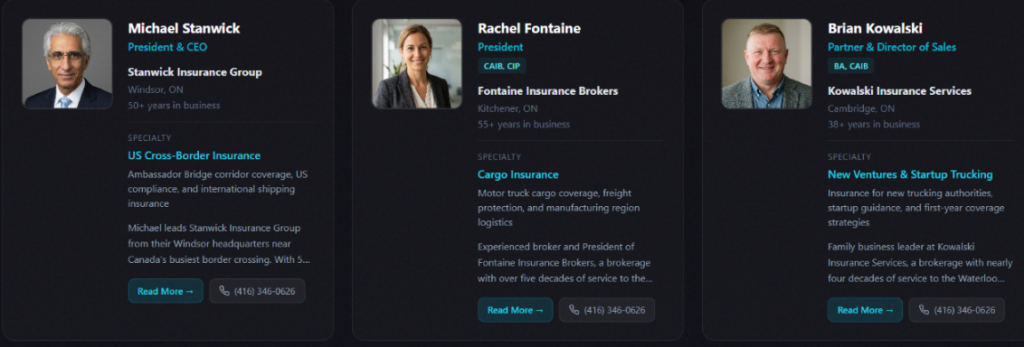

An Ontario-based company offering trucking insurance quotes is raising concerns after multiple licensed brokers said they’re not affiliated with the operation, despite being listed on its website as part of its network early yesterday morning. Those same brokers saw their names and profiles replaced shortly after inquiries were made on April 23.

The site, operating under the name Ontario Trucking Insurance, presents itself as a network of licensed professionals and directs users to submit information for quotes. But at least three of the nine Ontario brokerages whose profiles were initially displayed told CU‘s companion publication trucknews.com they have never heard of the organization and did not authorize the use of their names, images, or office details.

The Richmond St. headquarters address listed by Ontario Trucking Insurance actually belongs to Mitch Insurance, which surprised CEO Adam Mitchell (screen capture).

Those images, contact details and bios were included on a page that read, “Our Expert Team: Meet the licensed Ontario insurance brokers who write and review our content. Each expert brings decades of experience in commercial trucking insurance.”

“I have never heard of them,” said Ian McCowan of D.G. Dunbar & Associates, one of the nine experts listed.

Likewise, Joanna Mendonca, president of Staebler Insurance, said she is “not familiar with the organization” and does not recall providing any permission to be listed. “I believe I have never had any dealings or affiliation with them,” she added, describing the situation as “suspicious and concerning.”

Staebler and Dunbar were among four identifiable Ontario brokerages whose addresses were listed on the site’s contact page, although McCowan indicated the photo shown was not of him. Screen captures of the web page were taken, but only after site’s owner altered the ‘team’s’ photos and contact details.

RIBO reaches out

Adam Mitchell, whose firm was also listed on the site, said the first he heard of it was when the province’s broker regulator, the Registered Insurance Brokers of Ontario (RIBO), contacted him April 23. RIBO asked Mitchell if he had authorized the use of his name. He said he had not.

“It didn’t ring a bell,” Mitchell said of the company. “Once I saw the team and the makeup of a bunch of people, I knew there was no chance somebody had built a conglomerate of those people that are all still actively operating.”

It would’ve been a dream team of Ontario insurance professionals, he noted.

Mitchell said the site used his firm’s downtown Toronto office address, but reiterated had no connection to the operation. Ontario Trucking Insurance had no address of its own listed. But it did have a phone number. Trucknews.com called that number and received a recording saying: “Thank you for calling Trucking Insurance Quoting” and requested the caller leave their contact information “so we can get back to you as soon as possible to help you get a quote.” Trucknews.com submitted a form requesting a quote for coverage for a one-truck owner-operator, which as of press time had not been acknowledged.

A search of RIBO’s online registry tool did not return any brokerage operating as Ontario Trucking Insurance. Licensed brokerages in Ontario are required to maintain a physical place of business and have a verifiable address on file with the regulator. The website not only claimed the entity was RIBO-registered, but also indicated it was a member of the Ontario Trucking Association (OTA).

OTA told trucknews.com the company was not a member.

The domain for the website was registered in December 2025, according to public WHOIS records, which did not include the website owner’s name or contact information.

The website itself changed during the course of reporting on April 23, replacing a set of named brokers seen earlier on April 23 with another. The original nine Ontario brokers were replaced by nine new faces, some of whom appear to be U.S. insurance professionals, although some return no public profile. The phone number alongside each of their bios was that of Ontario Trucking Insurance.

In the late afternoon of April 23, the ‘Team of Experts’ page which originally featured Canadian brokers was replaced with new images of brokers, some of whom appear to be U.S. based. Phone numbers below each broker profile go to Ontario Trucking Insurance (screen capture).

There are several possible motivators behind the site. It could be intended to leverage the experience of legitimate insurance brokers to sell non-existent policies, leaving insureds uncovered. It could be used to generate leads, which the site owners could then sell to licensed brokers. Or the entity could be brokering insurance without authorization.

Mitchell said the biggest concern in being linked is not just reputational, but the potential impact on fleets seeking coverage.

“The one [thing] you’d hate to see is an honest customer that thinks they’re actively buying insurance for an incredibly expensive product and then finding out they have no coverage,” he said. “Cargo is not something you mess around with.”

He noted that periods of economic pressure can bring an increase in questionable activity in the insurance space, including fraudulent documents and misrepresentation.

While it’s not clear who is operating the website or how submitted leads are handled, industry experts say fleets should take steps to verify who they are dealing with before purchasing coverage.

Mendonca recommends checking the RIBO registry to confirm that both the brokerage and individual broker are licensed and active.

“That would at least confirm that the broker or brokerage is an active, licensed person or company,” she said.

James Menzies is Executive Editor of Today’s Trucking and trucknews.com. This article first appeared on trucknews.com, a companion publication of Canadian Underwriter.

The Municipality of Jasper will spend more than $2 million to replace wildfire-damaged curb stop valves in Cabin Creek Drive, Lodgepole Street and Miette Avenue neighbourhoods.

On Tuesday (April 21), council amended the capital budget to include this first phase of repairing utilities. The curb stop valves were damaged by firefighting, debris management and utility replacement activities during the wildfire.

The first phase will be funded through $1.5 million in provincial recovery funding and $510,000 from the utility capital reserve.

Council will decide on the $7-million second phase at a future meeting. This phase will focus on the remaining fire-affected blocks, including the 700 block of Connaught Drive; 700, 800 and 900 blocks of Patricia Street; and 800 block of Geikie Street.

CAO Bill Given said provincial recovery funding would likely cover repairs on wildfire-affected properties during the second phase.

“The bigger challenge is the other parts that are not exclusively fire-affected properties or that support main municipal infrastructure that’s also life-cycle replacement,” he said, referring to the aged sewer and water mains that need replacing.

Administration is now working on a report with more details and alternative funding strategies for phase-two work, which will be presented to council at a future meeting.

Housing loan guarantee

Council gave the first two readings to a loan guarantee bylaw that would allow the Jasper Municipal Housing Corporation to secure a $14.2-million federal loan for the Connaught affordable housing development.

The guarantee would specifically apply to a $5-million forgivable loan and a $9.2-million repayable one from the Canada Mortgage and Housing Corporation (CMHC).

Council still needs to give third reading to the bylaw at a future meeting.

The $21-million housing project would create 40 below-market units and is the first residential project undertaken by the Jasper Municipal Housing Corporation.

Land purchase

Council approved purchasing 1249 Cabin Creek Drive for $355,000 to potentially use for developing affordable housing.

Administration evaluated 1249 Cabin Creek Drive as a “high-priority acquisition” since it was properly zoned, serviced and cleared of wildfire debris.

The Municipality already owns 1251 Cabin Creek Drive, an adjacent property that had its house destroyed in the wildfire. Last week, Given said the purchase will create an opportunity to redevelop using these two parcels together.

The purchase will be funded through the community housing reserve.

Marsh’s global insurance market index (GIMI) report, a proprietary measure of commercial insurance rate changes at renewal, finds insurance rates in Canada declined 6% during Q1 2026, compared to a 7% decline in Q4 2025.

Property

Looking at individual sectors, Marsh’s report says property insurance rates slipped 6% during 2026’s first quarter and that competition levels are high. By contrast, rates fell 8% in the final quarter of 2025.

Marsh adds surplus capacity and strong insurer appetite in the property market led to rising levels of competition. “Most quota-share placements were over-subscribed, contributing to greater concurrency of key deductibles and sub-limits,” the report adds.

Insurers also relaxed policy conditions in order to secure business, “broadening terms to offset downward rate pressure,” Marsh notes.

Access to facilities helped clients seeking to improve their terms and/or costs. And the report says some clients redeployed premium savings into purchases of additional limits or lower retentions – “drawing on excess capacity and facility access to improve program structure and reduce cost.”

Casualty

Overall casualty insurance rates in Canada decreased 5% in 1Q 2026, matching the decline in 4Q 2025 and marking the 11th consecutive quarter of declines.

“Clients with Canada-specific exposures seen as good risks by insurers typically benefitted from expanded capacity and price competition,” the report says. But it adds risks exposed to the U.S. and other complex risks did see selective rate increases – some of which were double-digits.

For example, U.S. auto liability underwriting tightened, with higher attachments, shared loss structures, and telematics requirements for clients with those exposures.

Meanwhile, reinsurers emphasized limit management, higher attachments and reduced line sizes for accumulation risks. Scrutiny around underwriting also increased, “with a focus on higher attachments, sublimits, and/or per- and polyfluoroalkyl substances (PFAS) and pollution wordings.”

“Underwriters scrutinized PFAS and wildfire risks, at times using exclusions, sublimits, and mitigation-linked pricing,” the report says.

Depending on the specific risk, some clients emphasized fleet safety, telematics data use, and wildfire mitigation to improve terms and renewability, Marsh says. And, much like property clients, casualty clients also deployed premium savings into “additional casualty tower capacity.”

Professional lines

Rates for financial and professional lines in Canada declined 6% in 1Q 2026, slightly ahead of a 5% slip in 4Q 2025.

Marsh’s index notes rates for directors and officers liability coverage experienced a low single-digit decrease. And while rate reductions continued in some program layers, the report says insurers generally resisted further decreases.

“Rising fiduciary litigation tied to health and welfare plans is being watched, though without material impacts to underwriting or rates to date,” Marsh’s report says. And, “employment practices liability rates and exposures remained stable.”

Cyber

Rates for cyber insurance decreased 5% in 1Q 2026 in Marsh’s index. Capacity among insurers “expanded across excess and primary layers, including from new market entrants, increasing competition,” the report adds.

What’s more, there was continued coverage expansion and fewer coinsurance requirements and broader sub-limited enhancements.

“Organizations with strong cyber controls were well-positioned to negotiate lower retentions, broaden coverage, and capture excess-layer savings,” the report says.